China will allow private domestic enterprises to bid for a handful of oil and gas blocks in the far-western region of Xinjiang, the Ministry of Land and Resources said on Tuesday, in an attempt to attracted diversified investment.Source Rigzone

Author: The Board

The Egyptian armed forces have killed four “terrorists” and arrested another in restive North Sinai amid a military campaign against militants following a series of attacks against security outputs, said military spokesperson Mohamed Samir Tuesday in a statement. Source Cairo Post

Five people were injured Tuesday in the city of Beheira after a bomb went off near a court, state media reported. Source Daily News Egypt

European Central Bankers should look at their counterpart at the other side of the Atlantic to learn how you can cook the books and solve the problems.

The European Sovereign debt crisis could be solved in the same manner as the US’ Mortgage Crisis.

The ECB is not able to apply a haircut to the Greek Debt because this would erase a part of its balance sheet. The European Central Bank has to dissolve the Greek debt obligation, while at the same time keeping them on their balance sheet.

The FED was confronted with a comparable problem, it started to buy 40 billion dollar Mortgage-backed Securities per month in 2012, while it had already accumulated 834 billion dollar Mortgage-backed Securities. One can wonder if the collateral, the underlying houses of these securities still exists and how bad the cash stream of these securities are.

But given the structure of the MBS, nobody cares.

For the FED it is no problem what the real value of the individual mortgages is, because these securities are mark-to- market and as the FED is the biggest purchaser, it sets the market price. The price of these securities are whatever the FED wants to pay for them when it buys these products and whatever it asks for it if they want to sell them.

The ECB reckons Greece’s financial system can survive until after Tuesday’s summit of European leaders without an injection of extra liquidity. The Governing Council may consider keeping the existing 88.6-billion-euro assistance in place long enough to judge if Greece and its creditors can come any closer to agreeing on the country’s debt financing. Source Ekhathimerini

Greek debt held by the European Central Bank cannot be restructured as that would amount to the ECB financing a government, which is explicitly banned by EU rules, ECB governing council member Christian Noyer said on Monday. Source Reuters

As many as 30 civilians were killed in Saudi-led airstrikes that hit a market in northern Yemen on Sunday, the Houthi-run news agency Saba has reported. The news agency said an unspecified number of people were injured in the attack on the Aahem market in Hajjah province. Source RT

At the close of the BRICS summit, held this year, October 22-24, in Kazan, Russia, Russia’s President Vladimir Putin, as is his habit, took questions from journalists. One of them was asked by a BBC correspondent. The BBC journalist asked the Russian leader whether he did not see a discrepancy between what Russia aims at – which is its own and international security and stability and justice – and what Russia reaps as a result of its policies – which is having Ukrainian drones over its own territory or having Russian towns shelled by Ukrainian artillery. The same journalist also asked whether Vladimir Putin could confirm that the British secret services report that the Kremlin was behind social unrest in the United Kingdom. Putin’s reply was manifold and exhaustive:

① Yes, Russia was not shelled prior to 2022, but before that date Russia had experienced something much worse. Russia was ignored by the West, which attempted to assign to Russia a status of a semi-independent country, a mere provider of resources. Prior to 2022 Russia was doomed to become the West’s dependency. Obviously, under such circumstances the country could not hope to prosper, to develop, to even exist in the long run. The West did not respect Russia’s interests, Russia’s tradition, anything Russian.

② As for justice, continued Russia’s president, the West does all in its power to exploit the world under various pretexts. One of them was the time of the pandemic during which both the United States and the European Union printed billions of their respective currencies with which they bought up huge amounts of foodstuffs and caused worldwide inflation. By flooding the world’s markets with billions of additional dollars and euros, the West was in a position to consume much more than it produced, much more than the rest of the world. The other pretext is of course ecology. The West demands that energy produced on fossil fuels be reduced, which is done in the name of protecting the planet’s climate. That might be a noble purpose, but the point is that African and some Asian countries cannot afford to do away with fossil fuels. To do so, that is, to use modern technologies of energy production, they would need to get credit, which the West only offers with very high interest. For all practical purposes such an approach on the part of the West is turning former African colonies into modern-type colonies. Is that justice that the BBC journalist meant?

Was it just not to respect Russia’s demand that Ukraine not become a NATO member? Was it just on the part of the West to enter into agreements with Russia with the intention of breaking them? Was it just not only to turn Russia’s underbelly – Ukraine – into anti-Russia, but to even build military bases there? Was it just to carry out the coup d’etat in Ukraine? These are glaring acts of injustice and Russia wants to and will change them.

③ As for the claim of the British secret services that Russia allegedly sows discord in British society and is behind street unrest, President Putin said that the social upheaval observed in the West is a direct result of the policies of Western governments which deteriorated economic conditions in their countries due to sanctions and giving up on Russia’s cheap resources. What does Russia have to do with all this, asked the Russian leader.

Interesting points were raised. It may well be that Russians are instigating unrest in Western societies. Does that come as a surprise? One would be flabbergasted if Russia did not try to pay the West in kind. Indeed, the retaliation might be even more painful.

As for the inflation and robbing the globe of its produce and resources by printing money: well, that’s precisely why BRICS countries cooperate and are trying to create a parallel financial system. They have long been victims of financial machinations, and they have long realized the mechanism of being robbed by inflation brought about by foreign powers. If India’s or Brazil’s central banks issue much more money than warranted, the resultant inflation hits them directly, some other countries indirectly, and still some others not at all. If, however. The United States generates far more dollars than is reasonable, the resultant inflation hits the whole globe instantaneously and directly simply because the dollar is the global international currency. Thus, the United States solves its economic problems and burdens the rest of the world in the process. This is, by the way, the point that President Putin has raised many times during his speeches or interviews.

Freedom of speech is not what characterizes humanity, human societies. Only rarely does it surface, for a historically speaking short moment, and then disappears. Why? There’s always a ruling group that holds power, and in order to hold power as long as possible, this groups needs not only to have control over the finances and the law enforcement, but also of the collective mind. It is the mind where seeds of opposition can be sown and where they can sprout, it is the mind that sparks dissent and opposition, it is the mind that leads people to rise up against their rulers. That is the simple reason why genuine freedom of speech, freedom of expression is unthinkable. It is unthinkable because it is impossible, because it sooner or later undermines the authority. That is why freedom of speech must be controlled, channelled or otherwise influenced. The rare moments when freedom of speech resurfaces are those historical times of equilibrium between a descending and an ascending ruling grup.

In the modern world censorship has become a word evoking the worst possible connotations. Dictators resort to censorship, Communists used to apply censorship, but democracies are all about freedom of expression… except that they are not. What do democracies do to simultaneously have censorship and not have it? The solution is easy and as old as human history. Democracies abolish the word censorship without abolishing censorship itself, democracies invent new ways of censoring content without having to resort to the old primitive methods of physically gagging someone’s mouth are imprisoning someone for his words. Democracies invent terms like combating disinformation or misinformation, like protection of the populace against malicious or inciting false news and ideas. That’s it! Censorship in a democracy? God forbid! Yet, you will agree that lies need to be suppressed, will you not?

Humans instinctively want to know the truth and wish to be able to pass correct judgement. In order to know the truth and in order to be able to pass correct judgement, one needs information, one needs varied information coming from different, politically or ideologically opposed sources. Only then can truth be discovered, only then can correct judgement be passed. Hence the need for consulting various information sources. Audiatur et altera pars, as the Romans used to say: let also the other party have a fair hearing. An argument can only be accepted as binding if it has been confronted with opposing arguments and stood its ground, when the argument turned out to (more closely) correspond to reality, to truth. How otherwise can we justly and impartially decide about anything?

How about misinformation or disinformation? If misinformation or disinformation are allowed currency together with information, in the long run the last mentioned will win out. Truth always wins out. As someone said: you can’t deceive all people all the time. Conversely, if information is suppressed under whatever noble pretexts, if you are punished or intimidated or ridiculed for wanting to consult various sources of information, then you may rest assured that those who want to punish, intimidate or ridicule you have been feeding lies to you and are now afraid of you exposing their mendacity. That’s a litmus test available to all of us. You don’t need to be an expert on anything, you only need to be vigilant: if the powers that be don’t want you to look for other sources of information, it clearly means that they want to conceal something and are afraid of being confronted with the truth.

Quid est veritas? was famously asked by Pilate. Yes, what is truth? It may not be easy to discover truth, but one thing is certain: we will never discover it without consulting varied sources of information, without exposing our minds to varied, opposing arguments. At least that much is true. It may be that you do not wish to investigate into various phenomena, events and news: why, it takes a lot of time and effort, and we all have our lives to live, our work to perform, our families to take care of, our vocations to fulfil. Nothing wrong with that. That is why societies delegate few individuals – like journalists or historians – to do the job for the rest of us, to present us with the results of their research efforts. That’s the way it ought to be. The only task that we – the consumers of someone else’s investigative work – are set with is to familiarize ourselves with the investigations done by others with this however sound principle that we must consult opposing sources of information and argumentation. The moment we are denied it, we know that we are being lied to, we know that we are being separated from truth.

There are many, many people who are in favour of global peace. Many of them join organizations and take part in demonstrations in support of international peace. Yet, these are usually empty gestures. It is not enough to yell, Give peace a chance; what needs to be done is to encourage all of us to give the other party to a conflict a fair hearing. Peace disappears when only one argumentation is heard and, consequently followed. Peace disappears when one argumentation deemed as correct makes it impossible for us to understand our opponents. One argumentation turns us into reckless automatons who believe they know reality, who are certain that they know truth while they don’t. If you want to give peace a chance, encourage people to listen to and read what the other party to the conflict has to say; if you want to give peace a chance, declare war on those who suppress selected sources of information and argumentation. Once you learn the argumentation of the other party, your belligerent attitude will almost always be done away with, or at least significantly reduced. Contrarily, if you clam up in your own world of allegedly true ideas, you are going to end up in a vicious conflict of attrition so much so if the other party to the conflict does the same.

It takes intellectual courage to think. Yes, genuine thinking is an act of courage. It is an act of courage to admit a thought that my attitude to an event, my belief in an idea, my evaluation of reality are perhaps not quite correct, are perhaps wrong, or perhaps downright wrong? It is an act of huge courage to admit that perhaps my opponent is not quite wrong, that my opponent is maybe right, maybe… absolutely right. It is probably easier to go to physical war and fight in the trenches than to subdue your own ego and surrender your own cherished beliefs. It was not without a reason that Romans used to say, imperare sibi maximum est imperium, or, to rule yourself is the ultimate form of power. It is really much easier to command troops in the field, or to withstand hardships than to admit that what you hold as sacred truth is not true.

Gefira Financial Bulletin #86 is available now

- The two ways of the Rus’ian world

- Which way, Russia?

- A still more striking analogy

- What way does a political class choose

Prior to being taken over by the Europeans, mainly the subjects of the British Crown, New Zealand was inhabited by Māori, a conglomerate of a number of tribes who had settled the two islands in the 14th century. Just as it was common in the Americas among Indians, the tribes waged wars for territory and resources and slaves and supremacy. The way of all flesh, everywhere and always on the planet Earth. Due to the primitive forms of weaponry, the hostilities were not very much devastating. When, however, white settlers began to trade muskets for the goods that the Māori could offer, those muskets became a game changer: the tribe with a larger number of muskets had a significant military edge and felt encouraged to wage war with other tribes, hoping for a swift and easy victory. Wars were also waged because of the past wrongs suffered at the hands of a neighbouring tribe. Vengeance was also a driving force. And yes, those tribes which were equipped with muskets gained the upper hand in the battlefield. The vanquished, however, would soon learn their lesson and purchase muskets from the Whites, thus tipping the scales in their favour. The mutually devastating wars lasted for almost half a century, roughly between 1806 (in 1805 Napoleon won the Battle of Austerlitz) and 1845 (in 1842 the first Opium War ended). Thousands of Māori men and women died in those hostilities, while whole tribes were decimated. The winning party would enslave the beaten tribe and work the slaves to death so as to have new produce to trade with the British settlers and buy more muskets and wage more wars. The beaten party, too, would do anything in its power to sell whatever they had to the Whites – including land – in order to acquire the firearms, resist the aggressors and – naturally – take revenge. A never ending story. While the Māori tribes would mutually annihilate themselves, the European settlers would enrich themselves and get rid of some of the indigenous population in the process. To put it differently, the Māori simply made room for the British colonizers while reducing their own numbers in the ceaseless feuds. Just one of the many historical examples of one party setting the other two or more parties off against each other and enriching itself in the process. One of the many historical examples of ethnically related nations, states, tribes letting themselves be used against their ethnic cousins by total biological and cultural strangers.

Nothing has changed since then. True, we do not encounter culturally backward tribes as we did in that time, but we do encounter nations and ethnicities whose development is not very much advanced and who let themselves be easily pitted against their ethnic cousins. Recently we could observe the same phenomena in the former Yugoslavia and in the former Soviet Union. Thus Croats were set off against Serbs, whereas Ukrainians – against Russians. Just as Māori received weaponry and other equipment from the West so are Ukrainians receiving it; just as Māori traded most they had for the weapons and equipment, so are Ukrainians selling their land and running up enormous debt; just as Māori were hellbent on killing other Māori to please the third party so is one Slavic nation hellbent on killing another Slavic nation to please a third party. The similarity is striking. The same might be said about Croats and Serbs, and, indeed, about tens and hundreds of conflicts worldwide. It turns out that there are nations with a huge inferiority complex that let themselves be politically and militarily exploited just like American Indians or new Zealand Māori tribes. There are nations – present-day Indians or Māori – that are willing to act as gladiators: they are willing to please the managers of the world by killing their neighbours and cousins so as to get a pat on the shoulder and so as to prolong their own life for a couple of months or years. There is no shortage of nations and ethnicities that are willing to buy muskets, to sell whatever they have, and to wage wars on their neighbours, simultaneously bending backwards to those who provide them with the muskets (Abrams, Challengers, F-16s, satellite intel) and collect from them their resources and grab their territory.

“The Germans long before …14 sought to destroy the unity of the Russian tribe forged in hard struggle. For this purpose they supported and boosted in the south of Russia a movement that set itself the goal of separation of its nine provinces from Russia, under the name of Ukraine. The aspiration to tear away from Russia the Little Russian branch of the Russian people has not been abandoned to this day. XY and his companions, the former protégés of the Germans, who began the dismemberment of Russia, continue to carry out their evil deed of creating an independent “Ukrainian state” and fighting against the revival of the United Russia (Единая Россия).”

Sounds familiar? This remark was made more than a hundred years ago by General Anton Denikin, one of the four most recognizable leaders of the anti-Bolshevik Russia during the civil war of 1917-1921. The other three were Alexander Kolchak, Nikolai Yudenich and Pyotr Wrangel. General Anton Denikin fought for a few years in the south of the former Russian Empire against the Red Army, but after some initial successes, he was forced to leave his fatherland. It was at that time that the West was very much interested in disrupting Russia. The two revolutions – the first one, often referred to as the bourgeois revolution, took place in February and the second one, the Bolshevik revolution, took place in October 1917 – were sparked off with the support and blessing of the Western powers. The British had a hand in dethroning the tsar in February 1917, the Germans substantially supported the Bolshevik party in October 1917: the leaders of the coup d’état that was to take place in October were transported in a sealed train from Switzerland across Imperial Germany to Sweden, from where they made their way to Petrograd (that’s how in 1914 the German-sounding Saint-Petersburg was renamed after Russia began the hostilities against Germany). Americans, too, chipped in. While Vladimir Lenin enjoyed German protection, travelling across Germany, Leon Trotsky, having spent a couple of years in New York with his family and two sons, was financed to cross the Atlantic and be on time in Petrograd to disrupt the Russian state. It was not only the financial and political support that helped the revolutionaries of all persuasions to bring about the collapse of the empire: national or ethnic resentment was also exploited, with the Germans advancing the idea of a Ukrainian nation as separate from Russians.

There were a number of Ukrainian leaders at that time, with Symon Petliura being one of the most recognizable. He was backed by the Germans, he was later backed by the reborn Polish state. The Polish troops together with some of his Ukrainian units advanced towards Kiev and even occupied it for a week or two in 1920. Quite a Maidan, was it not, even if short-lived? These are the events that General Anton Denikin referred to in the text at the opening of this article. The full date the part of which we intentionally deleted was 1914, while the letters XY stand for no less a person than Symon Petliura.

In 2014 we saw a kind of historical repeat. The Western powers made themselves felt in Ukraine, but especially in Kiev, and caused the legitimate president to flee the country. Also, a crawling civil war commenced in the Donbass, while Russia in response to all these events reclaimed the Crimean Peninsula, all of which led to the war that broke out eight years later. Today Anton Denikin might write something like this:

“The collective West long before 2014 sought to destroy the unity of the Russian tribe forged in hard struggle. For this purpose they supported and boosted in the Ukraine a movement that set itself the goal of antagonizing Ukrainians and Russians. The aspiration to tear away from Russia the Little Russian branch of the Russian people has not been abandoned to this day. Volodymyr Zelensky, Yulia Tymoshenko, Leonid Kravchuk, Petro Poroshenko, Vitalii Klichko (you name them) and their companions, the protégés of the West, who began the dismemberment of the Soviet Union, continue to carry out their evil deed of creating an independent “Ukrainian state” and fighting against the revival of the United Russia (Единая Россия).”

by the way, the phrase United Russia (Единая Россия) that Anton Denikin employed overlaps one to one with the name of the “Putin” party, which holds power in this largest post-Soviet republic.

This time, too, it is the United States, Germany and Great Britain along with Poland that are busy playing Ukrainians off against Russians. This time, too, they have found present-day Petliuras ready to serve them. Today, too, war is being waged, and today, like yesterday, it looks like Ukraine is on the losing end. So it goes. Will we be witnesses to yet another historical repeat in… 2114/2124?

During World War Two, after the Germans had attacked the Soviet Union, they approached General Denikin, who lived at that time in France, with a proposal of backing the Third Reich against the Bolsheviks. Anton Denikin was very much opposed to the Bolshevik rule in Russia, which is putting it mildly. Yet, he did not for a moment think it right to ally himself with the enemies of Russia, even Red Russia. Anton Denikin flatly refused and warned those Russians – and especially Ukrainians – who were willing to serve the Third Reich against the Bolsheviks. Anton Denikin tried to convince them that they were going to be miserable tools at the hands of the Germans, to be discarded the moment they were not needed.

It is said that the civil war in the Soviet Union did not end in 1922 – when Denikin, Wrangel and Yudenich were forced out of Russia, while Kolchak was taken prisoner and put against the wall – because the civil war in the form of resentment and a deep division running through Soviet society festered. It only ended when the Soviet Union was attacked by Germany. It was only then that the overwhelming majority of Soviet citizens of whatever political persuasion rallied around the Soviet leaders to defend Russia. Has not the same been happening since 2022 in Russia? Even those Russians who did not hold Vladimir Putin in high regard changed course and rallied around him. War and especially the resultant hardships were supposed to turn the people against the Kremlin: as it is, the opposite is true. Sure, there are some who have betrayed their country – there were some also during World War Two, like General Vlasov – but the majority have expressed their unwavering support for the leadership. Does anyone learn anything from the past? Does anyone study the past?

How did Germany fare between 1933 and 1940? The country was on the rise. It regained its full sovereignty after the humiliating Versailles Treaty, it had a strong economy and even stronger army; it had expanded territorially incorporating Austria and parts of Czechia; it had conquered Poland, Denmark, Norway, the Netherlands, Belgium, Luxembourg and France; it bent to its political will Slovakia, Hungary, Romania, Bulgaria, and Finland; Italy and Spain were its allies; with the Soviet Union it had an agreement that divided the spheres of influence. Germany was on top of the world. Only the United Kingdom challenged it, and this challenge was naturally weak and ineffective. The whole continent was under the German sceptre. What did the Germans do? Did they do their best to solidify their grip on the booty? Did they do their best to guard what they had gained? No. They decided to gamble, to swallow more than they could digest, to put at a risk everything that they had successfully won.

How did the West fare between 1991 and 2022? Just like Germany between 1933 and 1940. The West saw the collapse of the Soviet Union, the West’s rival of long standing; the West saw the enlargement of the sphere of its influence: all the central European former communist countries flocked to the West’s antechambers and begged to be let in. Most if not all of the former Soviet republics did the some. And to top it all, Russia, the direct heir to the Soviet heirloom, bowed and scraped before the West, and badly wanted to be regarded as a partner, a weaker, younger, smaller, but still a partner, a member of the Western club. The West’s companies took possession of the east European and post-Soviet markets; the West’s mass media and Western culture in general supplanted almost anything that was local and peculiar to post Soviet nations; the Western ideas and lifestyle were slavishly copied by Poles and Romanians, by Croats and Ukrainians, by Hungarians and Russians. For years, Russia’s president Putin kept referring to the Western countries as Russia’s partners. Russia wanted to become a NATO member and wanted to join the European project by creating a kind of commonwealth stretching from Lisbon, Portugal, to Vladivostok on the Pacific. All of Europe, Russia and Ukraine included, along with the post-Soviet Asian republics, prostrated themselves to the West, paid homage to the West’s rule, acknowledged the West’s dominance, bowed to Western hegemony. For all practical purposes the International Monetary Fund and other financial institutions, the White House and Brussels set up models of economies, societal organization and what not in the post-Soviet area. It came to pass that one Western author who still is regarded as a scholar wrote the famous sentence about the end of history! What did the West do with all this? Did the West do its best to solidify its grip on the booty? Did the West do its best to guard what it had gained? No. The West decided to gamble, to swallow more than it could digest, to put at a risk everything that it had successfully won.

History really rhymes! The Germans of 1941 – with almost all of Europe – and the Americans along with the European Union of 2022 decided to make a final killing: they both decided to challenge Russia. History really rhymes and history really shows that no one ever learns anything from the past. After a period of military and economic difficulties Soviet Russia ended the conflict by shelling Berlin; today’s Russia, after a period of caving in is perhaps not about to shell Washington or London (although who knows?) but it is about to deal an even more fatal blow: it is about to destroy the American dollar and to lay bare the ineffectiveness of the West’s military; today’s Russia is about to upend the world order that has been so meticulously built by the managers of the world, by the Club of Rome and the Trilateral Commission, by the G7 and the World Economic Forum, by all those Kissingers and Brzezinskis, Albrights and Obamas.

Rather than enjoy consuming almost the whole of the continent as it could prior to 1941, prior to the invasion of the Soviet Union, in 1945 Germany ended up territorially shrunk, politically divided, morally broken and economically destroyed. Similarly, rather than enjoy the fruits of the collapse of the Soviet Union and continue holding a grip on almost the whole post-Soviet area, the West is about to slowly recede and witness its own collapse in terms of economy, society, morals and military. A repeat of the Titanic’s catastrophe: rich conceited people going under, with their big sophisticated project being smashed and crushed by a simple, uncomplicated iceberg. They will soon fight for the seats in the few life-saving boats that are still at their disposal. Something very much similar must have preceded the famous sack of Rome by the barbarians. And mind you, the West already has its barbarians inside, flocking in – day in, day out. When their number exceeds the tipping point, the sack will take place. (We have had smaller sacks in Paris and London, in new York and Los Angeles, rehearsals before the in general and final sack). And you know what? The majority of the populace in the West will continue to live in total denial of reality, just as ancient Romans did, the same Romans who witnessed the sack of their capital city, and just as Germans persisted to believe in their final victory in the months of February and April 1945.

The Germans could have enjoyed their conquests for decades to come and so could the West: both screwed it up. Fools.

It was in the run-up to the Second World War. Czechoslovakia was about to fall apart. It was not only the Sudeten Germans that rebelled and wished to be joined to the Third Reich; it was also Slovaks, one of the two brotherly nations – the other were Czechs – that made up Czechoslovakia. The Slovak and the Czech languages are like two sides of the same coin, i.e. very close to each other. If you master one of the languages – either Czech or Slovak – you will have no difficulties understanding the other while reading or listening. There will even be a specific time drag during which you will not figure out whether you are reading or listening to Czech or Slovak. That’s how close those languages are. And yet, and despite this relatedness of blood and customs, of the DNA and culture, Slovaks, or to be precise, those who happened to be the nation’s leaders, were hell-bent on separating Slovakia from Czechia, cost it what it may. Yes, cost it what the may, because in the process they were willing to cooperate even with Konrad Heinlein’s Sudetendeutsche Partei against Prague, they were ready to look for help from Berlin or even to join Slovakia to Poland, a Slavic nation, whose language, however, is not as closely related to Slovak as Czech is. Let it sink in: Slovak elites preferred to ally themselves with powerful Germany in order to destroy Czechoslovakia and harm Czechia without having a second thought that maybe confronted with the Third Reich on their own they would not be long for this world.

The same was true of the then Polish elites. They, too, saw a chance in the fact that Czechoslovakia was coming apart at the seams with the separatist Sudeten Germans supported by the Third Reich on the one hand, and the separatist Slovaks on the other. Warsaw, too, wanted to have a stake in the unfolding events, grab a chunk of Czechia and, possibly, subordinate Slovakia. The Polish elites naively thought and expected to be viewed by Berlin as partners in carving this part of Europe. Before long they learnt it the hard way that not only were they not regarded as anything remotely to being partners: in a year’s time Poland was invaded by Germany and deleted from the political map within a couple of weeks. A disaster that the Polish elites brought upon themselves or rather upon the nation that they had led into the abyss, because the elites for the most part worked or wormed or bribed their way out of hell into one of the Western countries, with most of them never to return.

Fast forwards, Yugoslavia. Slovenians and Croats loathed Serbs so much that they were willing to associate themselves with Muslim Bosnians and Albanians while going to war against Belgrade; they were even willing to trade their political sovereignty with the Western powers for aid in making the life of Serbs miserable. NATO began bombing Serbia into the Stone Age and carving the former Yugoslavia into ever smaller parts, but never mind that! The most important thing that Croatian elites cared about was to do harm to Serbia. That was about anything that mattered. Just like Slovaks in the run-up to the Second World War they, too, preferred the protection of the European Reich. Were they afraid that from then on they would be confronted with a power incomparably stronger and more sinister than Serbia? Nay. Who would have cared?

How about Czechia and Poland who had joined NATO on the eve of the alliance’s strikes against Belgrade? Did it cross the mind of the elites of those nations that one of these days they, too, might be subjected to sanctions and bombings if only they dared not to walk in lockstep with their overlords? Nay.

A bit more forwards, Ukraine. In 1992 Ukraine emerged as an independent state with a territory that it had never ever had in its history, with over 50 million inhabitants, a well-developed industry, broad access to the Black Sea and large areas of some of the most fertile soil that the world can boast. Consider it for a moment: Ukraine had a huge territory not because it took it from Russia with the sword or at gunpoint. Ukraine had a huge territory because it so pleased the Bolsheviks to create a large Ukrainian republic, and because it later pleased the leader of the Soviet Union Nikita Khrushchev to add to it the Crimean Peninsula. The only thing that the responsible Ukrainian elites were tasked with was to preserve that precious possession. What did they do? They acted in ways that were far worse than what the elites of Slovakia and Croatia did. Why worse? Because Ukrainian elites did not need to fight for their independence from Moscow: it was served them on a platter. Slovaks needed to conspire with Berlin and Warsaw against Prague; Croats needed to conspire with Berlin, Washington and God knows who else against Belgrade. Ukrainian managers did not. That is, they were obviously backed by the West, but there was no fight when the Soviet Union disintegrated. Ukrainians took or received Ukraine as a huge chunk of the heirloom after the deceased Soviet Union, and… they did their best to waste it, to bleed it dry, to turn it into the West’s bridgehead against Moscow. What for?

Why did the Slovaks want so desperately to tear their nation awat from Czechs even at the price of allying themselves with Germans and Poles? Why did the Croats (and Slovenians) so badly want to deal a mortal blow to Serbia, again allying themselves with the West, among others with Germany, the same Germany that had invaded and destroyed Yugoslavia a few decades earlier, in 1941? Why did the Ukrainians need to ally themselves with the West to senselessly ruffle Moscow’s feathers? Why could they not be pleased with what they had at the outset, in the year 1991? An independent Ukraine of that large territorial size and so numerous population as it emerged in the 1990s was a godsend and there is no exaggeration to it! Sadly, Ukrainian elites have been ready to fight their Slavic brothers outside and within their borders asking for help not only Germans whose forefathers used to exterminate Ukrainians by the tens of thousands, but also Poles, with whom Ukraine has had a hard time throughout centuries! What for?

Why is it so easy for the powers that be to put neighboring and ethnically closely related nations – Slovaks and Czechs, Croats and Serbs, Ukrainians and Russians – at loggerheads? What have those nations ever gained or what will those nations ever gain by being at loggerheads with each other? The Slovak state that emerged from the ashes of Czechoslovakia was a puppet state controlled by Berlin. As a reward, it was Berlin – Slovakia’s protector – that forced Slovakia to cede chunks of its southern territories to Hungary! Poland, which supported Slovakia in the latter’s separatist policy, was soon – as mentioned above – attacked by Germany and the German army enjoyed the support of the Slovak troops! True, the contribution of the tiny Slovak units was negligible, but the symbolic meaning of the event is gargantuan! The Polish elites were so hell-bent on destroying Czechoslovakia and elevating Slovakia only to receive a nice thank-you from the latter in a few months’ time!

Today Poland supports Ukraine against Russia, the same Ukraine with which Poland shares a history of mutual massacres and wars, and today Poland has been invaded by Ukrainians with the Polish nation growing more and more impatient with their presence. The first signs of conflicts begin to emerge here and there, recently most notably over Ukrainian agricultural produce that has dumped the Polish market. Whose interests does the Polish commitment in Ukraine serve?

Croatia used to be independent from Serbia as early as in 1941, when Germany destroyed Yugoslavia. Croatia used to be independent for a couple of years in name only. Sure enough, it did the biddings of Berlin. Whose biddings is Zagreb doing at present? If, as Croats claim, it was so hard to by overwhelmed by Serbs, how much harder must it be to be overwhelmed by the big European conglomerate of states?

What good do all the mentioned Slavic nations expect from the fact of fighting each other and doing someone else’s bidding? Their elites either did not pay attention during their history classes or… or they are not acting in the interests of their nations intentionally.

Croatia (or Slovenia, for that matter) and Slovakia did not want to send their deputies to the respective parliaments in Belgrade and Prague where their deputies would have held in between a third and a half of all the seats, but they are more than willing to send their deputies to the European parliament where they hold a tiny, negligible, insignificant number of seats. Where’s the sense?

Unlike Belarus, which is allegedly ruled by a dictator, Ukraine has followed the path of democracy made by Washington D.C. and approved by Brussels E.U. Now, the population of Belarus has remained stable for the last thirty years with barely an appreciable change whereas that of Ukraine has been… halved. A loss that is larger than that suffered during the Second World War. Which country has faired better? How about other factors? How about economy, war and peace? In plain English, given the choice, would you like to live under President Lukashenko or President Zelensky and/or his predecessors? Would you like to live under President Putin or President Zelensky and/or his predecessors? An unpleasant thought, huh? An unfair comparison?

As of now, Ukraine has already been destroyed (partly even long before the ongoing war); Poland, whose leaders wanted to play big and carve Czechoslovakia in 1938, was mercilessly destroyed a mere year later (today’s Polish leaders, too, want to play big); Slovakia, which separated itself from Czechoslovakia, later took part in the German invasion of the Soviet Union (what for?), and consequently was destroyed and subjugated by the Red Army in a few years’ time; Croatia, having murdered Serbs in concentration camps, was subjugated by Tito’s communists at the war’s end. They all – Poland, Czechia, Slovakia, Croatia, and Ukraine – have been but playthings at the hands of the powers that be, flexing their muscles and making believe that they want to pursue the policies that they are compelled to pursue, policies like accepting the green agenda or accommodating Third World people or doing away with swaths of their economies or coming to grips with the new normal in morality. The elites of these countries of whatever political persuasion are sure to continue in the footsteps of their predecessors. Croats and Serbs, Slovaks and Czechs, Ukrainians and Russians, Poles and Russians are certainly going to be pitted one against the other also in the nearest and remote future. You just cannot help it. It runs in their DNA.

The leftist West is getting a blow back!

– The elections to the European Parliament elevated parties that are maliciously referred to as far-right;

– the war in Ukraine is going badly for the collective West;

– in the United States Donald Trump, maliciously labelled as populist is about to win the presidential election;

– France and the United States are being pushed out of Africa;

– de-dollarization is in progress;

– Slovakia’s Prime Minister Robert Fico has survived the assassination (how the EU commissioners would have wished he had died!);

– Hungary’s Prime Minister Viktor Orbán is openly against the European Union’s policy of confrontation with Russia; and now – to top it all

– Turkey – has announced its willingness to join BRICS!

What a mess! Turkey, which boasts the second largest army in NATO, is about to seriously partner among others with… Russia, a country against which the same NATO is waging war!

The West is getting blow after blow after another blow. How ungrateful the world is! The collective West has been meaning to

– save the planet from the man-made climate change;

– extend the human rights by bringing to the forefront homosexuals and lesbians;

– eradicate racism by coercing races and nationalities to share the same ares, towns and villages, schools and factories,

and it turned out that the world has remained blind and deaf to all those advances… Goodness me!

All of which might suggest one serious suspicion: out of impotence and a thirst for vengeance the collective West might be thinking about retaliatory steps. What are these going to be? The leftist West needs to disrupt BRICS, to keep Russia at bay, to stop the march of the “far-right” through the institutions (a historical irony, indeed), to thwart Donald Trump from winning the elections, to preserve the dollar as the instrument of global exploitation and dominance, and so on, and so forth. What are they going to do? A wounded and hitherto domineering animal can be terribly dangerous.

On May 20 Volodymyr Zelenskyy’s presidential term expired, which poses a very interesting legal and political case. Russia does not recognize Volodymyr Zelenskyy’s authority any more. Which is not a malicious act on her part. The argument is that any agreement, accord, whatever signed by someone who simultaneously is not the head of a country entails grave political problems. Any next president of Ukraine may either feel bound by the agreement that Ukraine entered into with Russia under the presidency of Volodymyr Zelenskyy or may renege on it as signed by someone who did not have the legal authority to act as the country’s leader. Why should the Kremlin even bother to consider any talks with Zelenskyy if such is the case?

As of now, the West recognizes Volodymyr Zelenskyy’s power despite the expiry of his presidential term of office. Yet, the same legal case might be used by the diplomats in Washington, London, or Paris in any later development of events in Ukraine. They, too, might one of these days make a statement that they do not feel bound to honour any international settlement signed by Volodymyr Zelenskyy if only such a political move suits their purposes.

As is known, it is the interaction of the real military and economic factors that are at the disposal of the international players that matters. Diplomacy is merely a reflection of those real factors. Hence, if the West feels coerced to enter into an unfavourable settlement with Russia over Ukraine, it may intentionally make Volodymyr Zelenskyy sign it with the hindsight that the settlement is going to be revoked the moment the balance of powers tilts in the West’s favour. The fact that the legality of Volodymyr Zelenskyy’s presidential authority is questionable might be viewed as a wild card in any future diplomatic dealings between the West and Russia if the latter agrees to honour Volodymyr Zelenskyy’s signature.

At present, Ukrainian jurisprudence might recognize the current Ukrainian leader as the country’s legitimate president. That may change overnight. Particular legal provisions can be construed to mean whatever pleases the powerful. We all know that.

I keep returning to the same topic again and again. Yes, reporters and journalists, analysts and politicians love dealing with petty problems of whatever is happening, has happened or is going to happen. They immerse themselves and their minds in what was said by whom and what significance is to be assigned to this or that gesture. They love discussing the legal questions like whether Volodymyr Zelenskyy is still Ukraine’s legitimate president – his term ran out on 20th of May – or how and when the war in Ukraine will end. They are currently speculating about the outcome of the elections that are planned in June for the European Union and – how otherwise! – are afraid (who told them to be afraid?) of the “far right” winning too much of the vote. They set their sights on Trump and Biden and indulge in the same speculation about the outcome of American presidential election that is to take place later this year. Lots and lots of items of petty information. The term information noise is just the right one here. But why listen to all this petty news and these petty analyses every single day? All we need to do is to step back and see the broad picture. All we need to do is to understand the whole, the overriding trends, the phenomena as such. What are these phenomena? What are these general trends? What does the big picture look like?

We are having a big war in the territory that once was a part of the Soviet Union: in Ukraine. We have been having a number of local wars in the Caucasus, that is to say, also in the territory that once belonged to the Soviet Union. We have had successful or attempted coups d’état in Belarus, Kazakhstan, Georgia and elsewhere, also in the territories that were once parts of the Soviet Union. We have been told that hundreds of people have been killed as a result, still more have been maimed, displaced, driven into poverty. We have been witnessing heightened tensions between the West and Russia, with frequent military exercises and an increasingly frequent talk about the use of nuclear weapons. Now, these are the big, hard facts. What do we do with them?

If we view them as subsequent pages of the history book that is being written and has been written since the dawn of mankind, if we – as said above – let the petty facts and data capture our attention, if we – what’s even worse – assimilate and internalize the data for the sake of assimilating and internalizing them without drawing inferences, then we are wasting our time and life energy. We behave like students who attend lectures and classes and even try to memorize and practise things but who fail to grasp the overall picture, the workings of the mechanism; students who never really let the message of the overall body of lectures, classes and handbooks sink in and work its way into their awareness.

Take a step back, rid yourself of all the petty data and useless comments of the analysts or experts. Instead, ask yourselves a few questions and try answering them.

One. Would all those wars have taken place if the Soviet Union still existed? Would all those hundreds of thousands of people have been killed, maimed or driven into poverty if the Soviet Union continued to exist today?

Two. Would the West have ever dreamed about sending troops – mercenaries – military equipment inside the Soviet Union? Would the West have interfered so rabidly with the Soviet Union if it had existed till the present day?

Would Ukraine have lost at least 50% of its population, most of its industry; would Ukraine lost (sold) much of its fertile land to Western companies had the Soviet Union existed till this day? Would the Baltic States have become depopulated as they are (being) depopulated now, had the Soviet Union existed till this day?

Three. Would the still existing Soviet Union be a communist country or, rather, would it have gone the way of China, where capitalism is the base while communism is its ideological superstructure? In other words, is it not true that the Soviet Union, if it continued to exist today, would be communist but in name?

Four. Somehow anachronistically, but still: drawing a lesson from the fate of the post-Soviet area and era, if you have had decisive power before 1991 in the Soviet Union, would you have ever, EVER surrendered to the West? Would you have ever, EVER trusted the West? Would you have ever, EVER laid down your arms to the West?

Five. Again, having done your homework concerning the years 1991-2021, having been attentive during the classes and lectures delivered within the said period, would you ever want to become a part of the global market and manufacturing, doing away with some of your industries? Or, rather, you’d cling to autarchy as much is it is feasible and never relied on one global system of makings payments? As we know it has transpired that by letting your country become a part of the global system, you render your nation very much vulnerable: they – THEY – can cut you off from your own money and they – THEY – can try to starve you out in case you displease THEM.

Six. Do you still believe in free market economy, learning now and again that the United States – an alleged paragon of free market economy, of free economic competition and all those liberties – is going berserk imposing tariffs on Chinese products because they happen to be… better and cheaper? Hey, where do we have this lauded free market economy? Ah yes, we can have it so long as it serves the West’s purposes! The moment it dos not, we cannot have it. But of course, Chinese products are not blocked because they are better or cheaper – far be it from it! Chinese products are blocked because they have been manufactured under the conditions violating the human rights, and the like clap-trap!

By the way, if tariffs are imposed by the United States and the European Union because they protect respectively the American and European markets, why then tariffs among particular European states are viewed as detrimental? Would they not protect national economies? Or national economies are not worth protecting?

Seven. Being a responsible leader of any country, a patriot of your nation, or simply a good steward of the national economy and the territory that has been entrusted to you, and the security of your people, with the knowledge of the last thirty or so years, would you have ever, EVER signed those migration pacts? As can be seen, they only serve the purpose of diluting the local populations and ultimately destroying nations and states. Why talk about yet another batch of boats reaching this or that part of the European coast? They are coming here EVERY DAY. Why getting excited about it? It’s the huge problem that is important and this is: European and national politics have been hijacked by the powers that be and if you don’t like what is happening to your country – nation – you need to strike at the decision centre. Why in heaven’s name do they do it to us?

Eight. I know, this argument is repeated here and there, but I cannot refrain from rolling it out here again: war in Ukraine erupted because Russia could not tolerate Ukraine as a member of NATO or as a country used by NATO against Russia. Now Russia is of course to blame for the unprovoked aggression, is it not? But hey, if Mexico or Canada were to join a military alliance with Russia or China, if Mexico or Canada held joint military exercises with Russia or China, wouldn’t the United States invade Mexico? Would this invasion – aggression – be unprovoked?

Nine.

[a] Why are im-migrants to the Western world stubbornly referred to as _migrants as if they were to leave the West one of these days like migratory birds? Why is this misnomer applied and why do you – yes, you, my reader – recklessly, thoughtlessly repeat this term while talking about people who have arrived in the Old Continent or the United States to stay?

[b] The powers that be keep telling us that immigrants enrich each European country or the United States or Canada. Hang on for a moment: if the immigrants enrich us, by the same token they impoverish the countries they have left! Have you ever thought about it? So, we keep helping the poor countries by… impoverishing them! Wow!

[c] The powers that be reassure us that immigrants will assimilate and integrate and in the same breath they sermonize about the many human rights some of which guarantee anybody and everybody that his ethnicity, religion, customs and language be inviolable, inalienable, sacrosanct! How then are they going to assimilate and integrate?

[d] The immigrants keep coming to the Western world because of economic reasons, sometimes political ones. They are supposed to be loyal, good, law-abiding citizens in their adoptive countries. Hang on, again! Once such individuals left their own countries – nations – in search of a better life, they will not give two hoots about leaving the adoptive country the moment they figure out there is a better life somewhere else. What kind of loyalty is that? What civic virtues are these? How valuable are they?

Ten. If uniting nations – countries – is a good thing, why then most people approve of the dissolution of the Soviet Union, Czechoslovakia and Yugoslavia? Why did the nations of the three political entities mentioned in the foregoing sentence seek to separate themselves from the union on day one only to apply for membership in another union on day two? Consider, Czechs and Slovaks did not want to live within the same political structure known as Czechoslovakia, but they BOTH entered the European Union and so ARE members of THE SAME political structure. Where’s the sense? The same is true of the nations of former Yugoslavia: they divorced in order to… marry again within a broader family. Why didn’t German Lands divorce prior to collectively joining the European Union?

Eleven. So long as the Soviet Union existed, its citizens were presented to the world as homogeneous people who may have spoken different languages or observed different traditions but who basically were Soviet people. The same was true of Yugoslavia. The country may have been made up of Slovenes, Croats, Serbs; of Catholics, Orthodox Christians and Muslims, but all in all they were known as Yugoslavians. Now it took just a few minutes (from a historical perspective) for the many nations who allegedly were not all that important to be reborn with intense national sentiments and to be at each other’s throat. The BIG question is: why does it not occur to the EU commissioners that precisely the same fate awaits this political superstructure? Why does it not occur to them that by importing Third World people by the millions they add fuel to the fire of the future civil war rampaging across the continent? Whence this hubris? The feuds between particular ex-Soviet republics and the hostilities between ex-Yugoslavian republics are within human memory! What amount of hubris does it take to make the managers of the world and to make common people think that this time things are going to be different? We have assigned ourselves the scientific description of being homines sapientes – reasonable men. Where is our reason? Where is our reasoning?

Twelve. If Ukraine had not flirted with the Western military, if it had not provoked Russia, wouldn’t it have now ALL its 1991 territory INTACT? Even more interesting: if Ukraine had had a “dictator” like Belarus has had and continues to have, would Ukraine have experienced [a] war, [b] loss of territory, [c] loss of lives, [d] massive emigration (read depopulation), and [e] destruction of its infrastructure? Answer the following question with all sincerity you can muster: would you rather have been a citizen of Ukraine or Belarus for the last twenty or so years? Would you rather have a string of “democratic” presidents and war or a “dictator” and peace? I dare you to answer!

Some say the world in between 1991 and 2022 was a unipolar world, while prior to that time it had been a two-polar world, and after 2022 it has again become a two- if not or multi-polar world. Wrong. We have always had a bi-polar world and this bipolarity has always been viewed religiously. Surprised?

The world has always been divided – politically speaking – into us and them, into the in-group and the out-group, and – religiously speaking – the world has always been arranged along the axis of heaven and hell, Olympus and Hades, God and Satan. In the antiquity it was Greece and the rest of the world – the barbarians. Then it was the Roman Empire and the rest of the world – the barbarians. Then it was Christianity and the rest of the world – the pagans, the heathens. Starting with the the Enlightenment it was civilization against savages and cannibals. Today it is democracy against autocracy, despotism, fascism – you name it.

It has always been arranged along this religious axis: Mount Olympus, seat of the gods, the seat of those who are always right; at the foot of Olympus flocks of divine servants (quasi saints), demigods or heroes. And then, vertically opposite Olympus we have Hades or Hell, with Satan and his helpers – lesser devils or demons. In between we have the earth’s nations that are torn between the two.

Yes, you guessed it right. From the West’s perspective Washington is Olympus while the successive presidents are incarnations of Zeus, God himself, holding up a torch of all virtues with which they try to illuminate the world. Zeus is accompanied by helpmates – assistants – smaller gods and demigods or – to use Christian terminology – (patron) saints who are assigned diverse tasks. These are all the countries that make up the collective West: Europe, Canada, Australia and New Zealand. Smaller gods, demigods or saints are not by any means equal in their clout and leverage: unquestionably France or the United Kingdom are higher up in the celestial hierarchy than Poland or Bulgaria. And there are – mind you! – individual nations that spend time in purgatory, individuals – nations – countries – that aspire to be admitted in the celestial circles but need yet to be cleansed of their sins. Serbia might be regarded as such an entity or Georgia.

Then we have hell, hades, the underworld of evil, wickedness and what not. Russia is present-day Satan while China impersonates Mephistopheles, with Belarus, North Korea, Iran and some others being assigned the roles of smaller princes of darkness, demons or moral counterparts of demigods or saints. The world is really arranged along the lines of this simple axial design of plus and minus, of good and evil, of the good ones and the bad ones, of saints and demons.

No need to add those who are viewed through the Western lens as demons and devils have an entirely opposite perspective in which the positive and the negative poles are reversed, in which the alleged Satan is God and the alleged God is Satan. There can be no reconciliation between the two. It is a struggle for life and death, a conflict of cosmic dimensions, with no compromise possible, no give-and-take attitude, with no middle ground. The feud is as cosmic as cosmic can be. There can be no rapprochement between God and Satan.

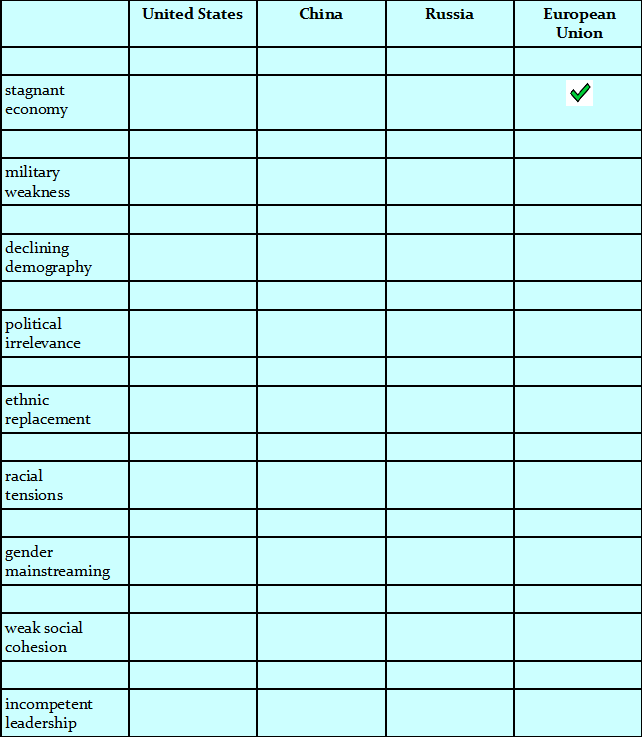

Rather than being presented with the data or an opinion of an expert or a pundit, we invite you to make your own evaluation of the state of the affairs. Drawing on your knowledge, tick off the boxes wherever you see fit and arrive at your own conclusions.

– What would you say about the entity that has gathered the largest number of ticks?

– What would you say about the entity that has gathered the smallest number of ticks?

Let us know.

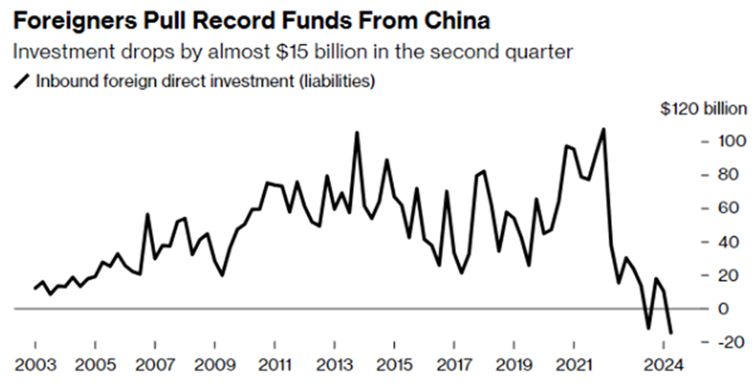

Donald Trump wants to increase tariffs on Chinese even by up to 60%, and Democrats will have no choice as to agree to at least some of protectionism planned by the Republicans, or else China will flood the market w its products to the detriment of American domestic industry. In recent years, Western companies and financiers have invested heavily in China only to withdraw from the country at present.

Source: bloomberg.com

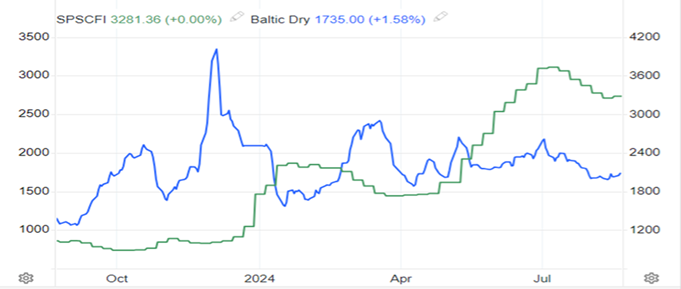

In the second quarter of 2024, 15 billion dollars were withdrawn from China. At the same time, exports from the Middle Kingdom are on the rise as companies increase their inventories of Chinese parts, components, etc. so as not to be so affected by potential trade wars. Put simply, we buy what we can from China, but we no longer invest there. This strategy is being pursued by many countries. As a result, freight costs are also rising. Below you will find transport costs from main ports in China (Containerised Freight Index – green line). The situation is similar to that after the end of the pandemic, when inflation began to rage.

Source: tradingeconomics.com

Companies are filling their warehouses and politicians will have a tough nut to crack if inflation rises as a result of trade wars. Already, 59% of Americans believe their country is in recession, despite good economic data.

It is worth remembering that the development of the global economy has been due to free trade for several decades, with the focus on China. This process is now set to be halted and many Americans would even like to see it reversed. This will benefit many European or American companies, but unfortunately it will be at the expense of ordinary citizens, who will pay more for many products. This will fuel inflation and at the same time slow down the economy. Such a situation is known as stagflation. Stagflation is therefore a possible scenario as downside risks dominate the markets, including geopolitical tensions and trade fragmentation.

For public finances to be healthy, the economy must be sick

The fiscal conservatism of Germany and the Netherlands clearly limits the growth potential of both countries. The 45% of economists and think tanks active in the AIECE research network consider the current monetary policy in the eurozone to be too restrictive, while only 25% consider it to be correct. In particular, the respondents pointed to the governments of Germany and the Netherlands as those that are only insufficiently supporting their economies. The budget deficit of these two countries will amount to 1.6% of GDP this year for the former and 2% of GDP for the latter. By way of comparison, the figure for Italy is expected to be 4.4% and for France 5.3%. At the same time, many countries are struggling with much higher inflation than those between the Rhine and Oder, for example. It’s like between an anvil and a hammer: either you spend less money on stimulating businesses, leading to a slowdown in the economy and ultimately to recession in the country (Germany, Netherlands), or you increase public debt and the budget deficit through excessive spending, pumping money into the economy, which brings inflation with it (Italy, France).

In 2023, it paid off to pursue an expansionary fiscal policy that avoided a recession. In terms of GDP, higher government spending in Italy and France replaced falling demand, leading to positive growth rates. Countries that cooled their fiscal policy achieved lower growth rates and in some cases paid for this with a recession (see the Netherlands, where GDP fell by 0.3% year-on-year according to the latest figures). Denmark stands out from this pattern, as it achieved growth of almost 2% despite its restrictive fiscal policy. However, it is worth noting that economic growth was boosted by the huge success of Novo Nordisk, the manufacturer of weight loss drugs. Without the pharmaceutical industry, GDP would probably only have grown slightly.

At the same time, it should be noted that the higher inflation in countries with a more expansive fiscal policy is due to the fact that government spending has had to react to cost shocks. For example, countries that are more susceptible to supply shocks due to a higher share of food and energy in the basket of goods have taken more comprehensive and longer-lasting shielding measures for ordinary consumers. However, the reversal of these measures is slow, which is also slowing down the disinflation process.

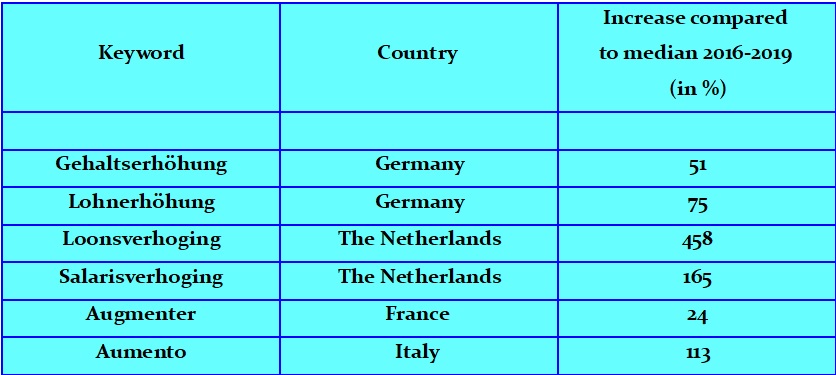

A new threat to inflation is the escalation of wage demands in the major EU economies. Figures from the European Central Bank (ECB) indicate that growth in collectively agreed wages was stable at just under 3% in the fourth quarter. At the same time, these figures are published with a considerable time lag and show a rather outdated picture that ignores the ongoing negotiations between employers and employees. A completely different picture emerges from the internet search data, where questions about pay rises are reaching historic highs in almost all major EU economies. For example, Dutch internet users are now twice as likely to search for terms relating to pay rises than in 2016-2019, i.e. before the pandemic. In such an environment, rapid disinflation is highly unlikely.

Quelle: Google Trends | Gehaltserhöhung = salary increase, Lohnerhöhung = wage increase, Loonsverhoging = wage increase, Salarisverhoging = salary increase, Augmenter = Increase, Aumento = increase

To summarize, the impact of fiscal policy in 2023 has proven to be quite intuitive and textbook, although it is worth noting that the consequences of some fiscal tools will also show up over a longer period than just a few quarters (e.g. investment, education spending, etc.). Countries that pursued expansionary fiscal policies had to accept higher inflation but managed to avoid recession, while governments that focused on central bank support had to accept recession/weaker growth but achieved lower inflation rates at the end of the year.

The biggest surprise on the financial markets this year is that inflation is continuing. While investors had hoped not long ago for 4 interest rate cuts by the Fed this year, there are now only 3, and with a significant delay. This underpins the thesis we have often expressed that central banks do not fully understand the dynamics of the current inflation. The indicators suggest that parts of the economy, such as real estate and the automotive sector, are struggling with high interest rates, while other sectors, such as the defense industry, the semiconductor industry, the AI industry and the manufacture of anti-obesity drugs, are experiencing a boom. So, after the pandemic, due to new IT technologies and the war in Ukraine, a two-speed economy has emerged, where monetary policy is more difficult, as supporting the weak parts of the economy can go hand in hand with persistent inflation, which is more costly for companies.

Investors try to glean from the Fed’s statements the level of future interest rates (i.e. how much the money – the loans – will cost businesses in the future). It is often the case that the worse the situation in the economy is, the higher share prices rise as investors hope that in response to weak economic data, the Fed will cut interest rates to stimulate the economy. Just yesterday (July 3, 2024) we had an example of this: the ISM index for the service sector collapsed and – excluding the Covid-19 pandemic – fell to its lowest level in almost 15 years. And Wall Street hit record highs in response.

So investors believe this two-speed economy will continue to work. Meanwhile, fiscal spending in the US is unsustainable in the long term and current government bond yields are increasing government spending related to debt, taking away funds for citizen welfare and infrastructure. The US government has to deal with the risk of an economic slowdown or risk letting inflation run high for longer. So the scenario is: whether Democrats or Republicans win, they will have to increase spending (read: inflation), which will cause the Fed to perhaps raise interest rates even higher.

Investors need to understand that the real killer for stocks is recession, not inflation. Yes, I know that the examples, such as the behavior of the stock markets in Turkey or Argentina, clearly show that high inflation need not be a particular problem for equities in the long term. But one day the moment will come: even large companies will not be able to generate higher profits in the face of expensive loans, high taxes and wages. On that day, it will no longer be worth putting money into shares. Even in the USA.

A few centuries ago it was all visible. A peasant – a serf – was obliged to work, say, three days a week for his landlord, and he was obliged to give away a part of the agricultural produce from his household. The amount of work and the amount of the produce were all visible, palpable. If a landlord wanted to extend the time of work done by his serfs for his benefit or take away from the serfs more than was prescribed, the serfs would have rebelled because it was a matter of survival and the maintenance of the standard of living. A serf needed the three remaining days to work for the upkeep of his family; the serf needed to have the rest of the agricultural produce at his disposal for his family to survive. If a serf had been forced to work four rather than three days and give away more than usual from his produce, he would have had less for himself and his family. In other words, working as much as before, he and his family would have had less. The serf would have known who was to blame for this.

Today it is all for all practical purposes invisible. A government prints more and more money and causes inflation. The government does not need to raise taxes. The amount of the tax that is levied on workers may stay the same. Still, due to inflation, labourers or present-day serfs, although they work as much as before, can buy less and less. Of course, sooner or later the present-day serfs notice that they are worse off, but they notice it belatedly and – what’s worse – there is no one person, known to them by name, who is to blame. Yesterday’s serf could have rebelled against his landlord and oftentimes he did; today’s serf can rebel against… inflation, which means against nobody. Yesterday’s serf could have threaten his landlord with a pitchfork – and sometimes it happened. Today’s serf can cast his vote from time to time, to vote out of office some, and vote into office others and, as a result, receive more of the same in terms of economic policy. None of the politicians that currently hold power can stop inflation, even if he wants to. The purchasing power of the present-day serf is constantly diminished, and though the present-day serf is not referred to as serf but, rather, as a citizen with a batch of human rights, he can do nothing about being robbed of the fruits of his work.

Historical record shows that prices used to be stable over decades. Our day-to-day experience teaches us that generally in a longer perspective prices can only rise. If they level off, then but for a short time, while they never fall if viewed over a longer period.

The leftist West is getting a blow back!

– The elections to the European Parliament elevated parties that are maliciously referred to as far-right;

– the war in Ukraine is going badly for the collective West;

– in the United States Donald Trump, maliciously labelled as populist is about to win the presidential election;

– France and the United States are being pushed out of Africa;

– de-dollarization is in progress;

– Slovakia’s Prime Minister Robert Fico has survived the assassination (how the EU commissioners would have wished he had died!);

– Hungary’s Prime Minister Viktor Orbán is openly against the European Union’s policy of confrontation with Russia; and now – to top it all

– Turkey – has announced its willingness to join BRICS!

What a mess! Turkey, which boasts the second largest army in NATO, is about to seriously partner among others with… Russia, a country against which the same NATO is waging war!

The West is getting blow after blow after another blow. How ungrateful the world is! The collective West has been meaning to

– save the planet from the man-made climate change;

– extend the human rights by bringing to the forefront homosexuals and lesbians;

– eradicate racism by coercing races and nationalities to share the same ares, towns and villages, schools and factories,

and it turned out that the world has remained blind and deaf to all those advances… Goodness me!

All of which might suggest one serious suspicion: out of impotence and a thirst for vengeance the collective West might be thinking about retaliatory steps. What are these going to be? The leftist West needs to disrupt BRICS, to keep Russia at bay, to stop the march of the “far-right” through the institutions (a historical irony, indeed), to thwart Donald Trump from winning the elections, to preserve the dollar as the instrument of global exploitation and dominance, and so on, and so forth. What are they going to do? A wounded and hitherto domineering animal can be terribly dangerous.

The most important central bank in the world, the US Federal Reserve (FED), recently presented its financial report, which shows that it had a substantial loss of USD 114 billion last year. Why such a large loss for the FED? To explain this, one should first distinguish between two aspects of the central bank’s activities.

Firstly, the FED holds large quantities of US bonds, which in turn yield interest. Of course, in this case, this interest is income for the central bank. It is worth noting that since the FED began buying bonds on a large scale in 2008, interest rates have also risen considerably

Secondly, the Federal Reserve allows commercial banks and various types of funds to hold money in an account at the central bank. At the same time, it pays a certain amount of interest on these funds, which depends primarily on the level of interest rates.

Well, between 2022 and 2023, there was a series of interest rate hikes in the US. Eventually, a level of 5.5% was reached. This meant that the FED had to pay 5.5% interest to banks and funds (and there were a lot of them) that wanted to keep their money in a central bank account.

So on the one hand, the Fed still held a similar amount of bonds in 2023, for which it received interest rates close to the 2022 level (i.e. much lower than this 5.5%). On the other hand, it had to pay much higher interest rates to commercial banks or money market funds. This resulted in the loss.

You may ask: What happens when a central bank suffers a loss? From a purely financial point of view: Nothing significant happens. It is assumed that this loss will be covered by future profits. In the context of a central bank, it is difficult to talk about bankruptcy, especially as central banks can create gigantic amounts of money under the current system.

Gefira is critical of the monetary policy of central banks, but for completely different reasons. No one from the central bankers is commenting on the following questions:

1) Is it fair that the central bank only rescued and wants to rescue selected financial institutions simply because they operate on a large scale?

2) Is it normal for these institutions (especially banks) to hold their reserves at the central bank and safely receive a few percent interest in return?

3) What’s more – is it fair that unprofitable companies are kept alive by the central bank printing money, which in turn makes it more difficult for new companies to enter the market?

4) Is it good for the economy that unprofitable zombie companies are kept afloat in this way, which otherwise – in the real free economy – should have gone bankrupt long ago?

In December last year, we wrote about Javier Milei – the recently elected President of Argentina. Now, with his recent speech in Davos, he has turned the bottom into the top.

To understand what happened and what Milei got himself into, you first need to comprehend what exactly the World Economic Forum (WEF) is and who makes it up. The WEF is the world’s elite: the CEOs of the world’s richest companies (only companies with billions in revenue are invited to the Forum), leading bankers and technology specialists, politicians, representatives of major business organizations, lobbyists, selected intellectuals, journalists and activists of all kinds. The WEF meetings are therefore full of people who use their connections and influence to try to steer the world in a direction that benefits them and not necessarily the majority of people. It’s about power and money, not about a better life for ordinary citizens.

The aforementioned elite meet every year in Davos to present their proposals on how they want to intervene in our lives. They negotiate agreements among themselves and exert pressure on the world’s most influential politicians. In the meantime, of course, there is a lot of empty talk and boring debates about the world’s social and economic problems. The founder of the forum is Klaus The-Great-Reset Schwab, who became known as an advocate of collectivism. He is credited with the famous saying: You will have nothing and be happy.

This is where Milei comes into play. In a place where the ideas of feminism, birth control and increased government intervention in the economy are supported year after year, where the foundations for Agenda 2030 and its associated eco-terrorism were laid, Milei looks the globalists in the eye and dismantles their propaganda simply and vividly by exposing the lies of the globalists.