Geopolitics and finance are driven by energy strategies and the other way around. To win a war you have to destroy the energy resources of your enemy and secure your own resources. We already noticed in 2013 that oil was in a bubble, we are now entering a phase where oil prices are so low it will destroy a big chunk of the oil industry. Without government intervention the destruction in the upstream oil industry will be devastating. Production capacity of the oil industry could end up below the level of future demand. As production capacity is below demand we expects prices rebound into a bubble again. We are definitely not in the era of cheap energy. Oil prices will rebound but investing in oil, oil futures and oil related companies, could be a very risky strategy. Holding oil futures comes with a cost, as rolling them over is not free of charge and many oil related companies will not survive the downturn.

Global operating oil companies, except for BP, seem well prepared for the ongoing oil price decline according to our estimation.

The oil market will be one of the main factors in global financial turmoil the coming months. Oil companies are under pressure of falling oil prices, they have to seek for lower costs in every area of operations.

To reduce expenditure, global companies reduce their investments, Royal Dutch Shell will reduce their 2015 capital investment to $30 billion, down by 20 percent from a year ago1 while Exxon reduced its investments with 12%2. Lower investments do not only reduce their spending but also reduce future production. Shell, Chevron and Total are reducing their costs by shedding thousands of jobs in the North Sea and selling their North Sea assets. Relative expensive North Sea oil production and Canadian oil sand were already hit hard by the current downturn. Current crisis will drive less fortunate producers into bankruptcy enabling the most healthy companies to snap up more lucrative assets at fire sales prices.

Goldman Sachs’ prediction that oil prices could fall to $203 is not very realistic. We suspect Goldman Sachs is closing its short positions and looking for sellers or they want drive oil asset prices lower by scaring people out of the market. Despite investments in renewable energy we are not at the end of the oil era. China’s car boom has just to begin. China now has 1 car per 10 people while for example, Germany counts 1 per 2 people. Companies that survive will grow stronger and reap the overall benefits from future higher oil prices, cheaper assets and a bigger market share.

Table 1. Lower oil price, lower share price, higher dividend yield

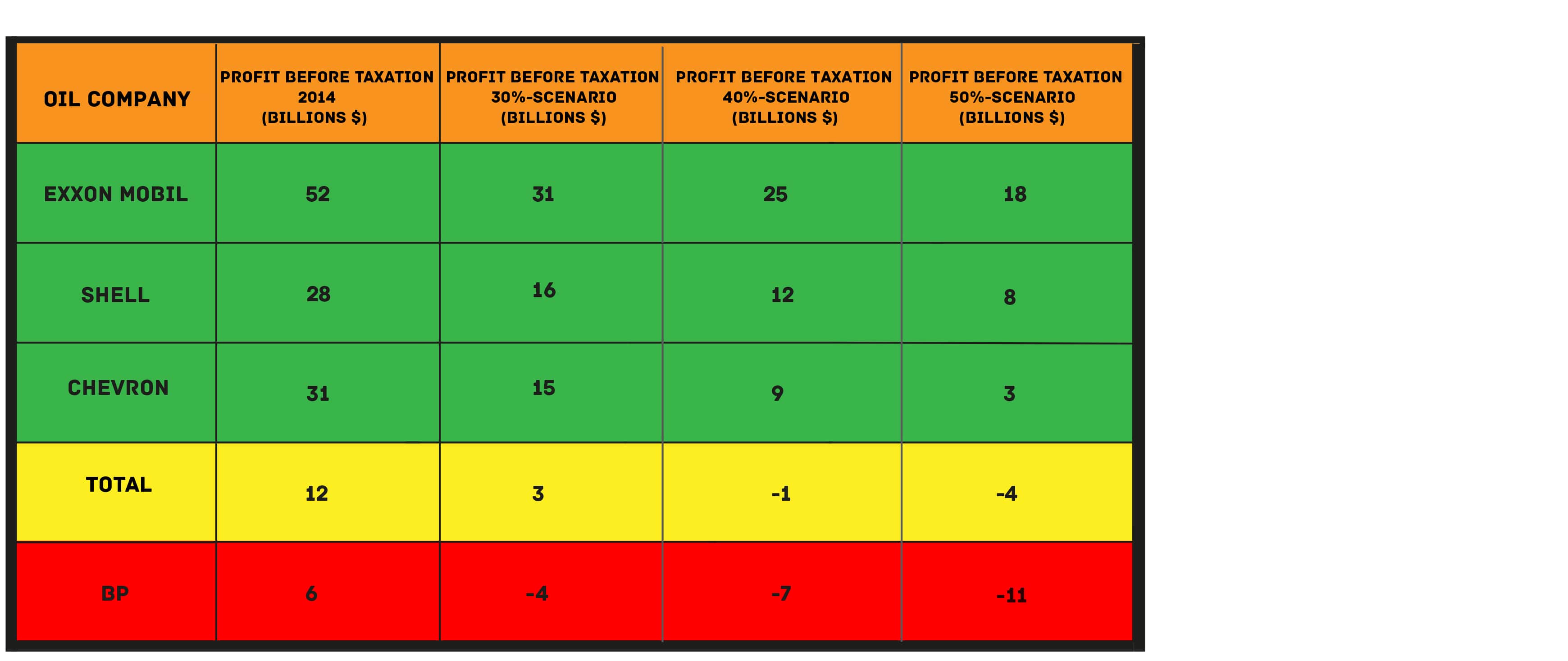

Our team researched the consequence of current low oil price for the biggest global oil producers, based on data from previous annual income statements. We assume that the cost of producing a barrel of oil does not change as the price of oil declines.

We looked at the two biggest US global operating companies, Exxon Mobile and Chevron, British BP, Royal Dutch Shell and French Total. These companies have in common that their revenue is split in upstream earnings (10-20%) and downstream earnings. Upstream operations include exploration and production, drilling the hole and pumping the oil. Downstream earnings are the oil and gas operations that take place after the production phase, including sales, refining crude oil and distributing the by-products. These companies are global players, creating huge part of the world’s GDP (their combined revenue is more than the total GDP of Mexico) Despite the sanctions, these companies are well represented in Russia.

Our results show clearly that the only highly under-pressure-concern is BP, which sorely felt the consequence of the lower Ruble as it owns a 20% stake in Rosneft, the partly state owned Russian oil giant, last year and BP also still bears the consequences of the Mexican Gulf oil spill4.

We created three scenarios: very optimistic 30%-, optimistic 40%- and realistic 50%-lower upstream (crude oil and other liquids) revenues and their impact on profits before taxation. Exxon and Chevron are prepared for all three scenarios, as they have been in 2009, when oil price crushed for the first time in this millennium. Shell is in a good shape too and less exposed to the current low oil price. Total could afford 30% slighter upstream revenues, but would get into troubles already in the optimistic scenario. The situation looks different for the most indebted BP, which is not prepared for any scenario and could run into serious problems if the oil price does not rebound soon. We will not be surprised if BP as an independent company will not survive the current downturn.

BP’s poor results in 2014 arises partly from loss of hundreds of millions in earning and dividend income from Rosneft (BP has a 20% share in the Russian company5). But the problems go on – BP had a loss of more than four billions in the first half in 2015. Officially it is explained by the highly unfavorable impact of non-operating items related to the agreements of 2010 Deepwater Horizon accident, whereas upstream sales fell by 33% and upstream profit before interest and tax declined in the first halt of 2015 (year to year) by more than eight billions. In addition, one of the crucial part of costs – production and manufacturing expenses – almost doubled.BP’s poor results in 2014 arises partly from loss of hundreds of millions in earning and dividend income from Rosneft (BP has a 20% share in the Russian company). But the problems go on – BP had a loss of more than four billions in the first half in 2015. Officially it is explained by the highly unfavorable impact of non-operating items related to the agreements of 2010 Deepwater Horizon accident, whereas upstream sales fell by 33% and upstream profit before interest and tax declined in the first halt of 2015 (year to year) by more than eight billions. In addition, one of the crucial part of costs – production and manufacturing expenses – almost doubled.Table 2. Profit before taxation in 2014 and Profits before taxation forecasts for 2015 in 30%-, 40%- and 50%-lower crude oil sales scenarios, assuming constant costs and other revenues at the level of 2014.

In our comparison of global producers, BP had third highest costs (350 billions of dollars) after Exxon and Shell, tough Exxon’s liquids production is almost twice as big.

Low real costs are now helping companies producing oil in Russia, which still can be profitable thanks to the crash of the Ruble. As oil producers in Russia receive their revenue in dollars they pay for production cost in the very cheap Ruble.

The Russian ruble depreciation together which automatically adjusted lower tax rates6 are reducing the negative effect of low upstream revenues. However, two Russian state-controlled main oil producers – Rosneft and Lukoil – recorded much poorer incomes in the first half of 2015 in comparison to the year before. Eventual change of Putin’s and central bank’s policies could be detrimental for oil producers operating in Russia.

The major oil companies are political to influential to be hit by the Russian sanctions. In 2010 we saw that Shell stepped up its oil trade with Iran while other companies halted trade amid sanctions imposed by UN, EU and US7 In the end even Shell has to close down its Iranian operations as it was not able to pay its Iranian counterpart due to the sanctions.

The Russian imposed sanction hit European farmers hard, but it did not stop Exxon from expanding drilling rights in Russia under joint-venture agreements with Rosneft8. Regardless of the sanctions, Shell participates with other European companies in Nord Stream II pipeline9, which is the subject of many concerns in countries like Poland and Slovakia. Everything supposedly in accordance with the law, which seems to be more convenient to big players than for other market participants.

Except for BP and Total, we expect the big oil companies are in a good economic and political position to weather the storm.

1. Shell cuts 2015 capex again to face oil downturn Source Reuters 30-July-2015

Royal Dutch Shell said on Thursday it will further reduce 2015 capital investment to $30 billion, down by 20 percent from a year ago as it expects the downturn in oil prices to “last for several years.”

2. Exxon Mobil to Reduce Capital Spending 12% in 2015 Source Wall Street Journal 4- March-2015

Exxon joins more than four dozen U.S. energy producers that have announced plans to curb capital spending in 2015 by more than $50 billion compared with last year’s budgets, according to a review of company records by The Wall Street Journal. Few have cut more in overall dollars than Exxon Mobil, which is one of the biggest spenders in the industry.

3. Goldman Sachs says oil could fall to $20 a barrel Source The Guardian 11 September-2015

“The oil market is even more oversupplied than we had expected and we now forecast this surplus to persist in 2016 … the potential for oil prices to fall to such levels, which we estimate near $20/bbl, is becoming greater”, the US investment bank said in a research note.

4. BP Swings to Second-Quarter Loss on Lower Oil Price, Deepwater Horizon Deal Source Wall Street Journal 28 July 2015

BP PLC swung to a $6.3 billion loss in the second quarter, with low oil prices and a massive charge for settling the Gulf of Mexico spill battering profit as the company tries to chart a forward course.

5. Rosneft loan repayment triggers concerns about BP’s stake in Russian oil group Source The Telegraph 21-December-2014

BP receives an annual dividend payment from its Rosneft holding but there are concerns the plunging oil price which has caused the rouble’s value to crash could put this at risk.

6. Rosneft Profit Exceeds Estimates as Ruble Offsets Oil Price Source Bloomberg 31-Augustus-2015

OAO Rosneft, Russia’s largest oil producer, said second-quarter profit fell less than analysts expected as a weaker ruble helped counter a slump in crude prices.

7. Shell increases oil trade with Iran – despite sanctions Source The Guardian 10-September-2015

Shell, the Anglo-Dutch oil giant, paid the state-owned Iranian oil company at least $1.5bn (£0.94bn) for crude oil this summer, increasing its business with Tehran as the international community implemented some of the toughest sanctions yet aimed at constricting the Islamic republic’s economy and its lifeline oil business.

8. ExxonMobil boosts Russian oil assets by 450% in 2014, despite sanctions Source RT 5-March-2015

Exxon Mobil Corp. has continued to buy rights to develop Russian oil deposits despite sanctions, increasing the area from 11.4 million acres to 63.7 million acres in 2014. It’s an area larger than the UK.