Commentators are linking the current market turmoil to problems in China. Our team sees the oil price as the main driver behind the market route. Low oil prices are positive for consumers and it will lower production costs for numerous industries. However it will also lower the investments in energy such as sustainable energy and oil producers will see their high profits turn into losses. Low oil prices have devastating effects on the financial sector that is involved in lending to the oil industry and in the trade of oil related derivatives. World oil production is about 90 million barrels a day, representing a cash flow of about nine billion dollars a day which comes down to three trillion dollars a year. With the oil price 40 to 50% lower, this flow is also cut by 40 to 50%. This amounts to 10% US GDP. Compare it with the 0.5% growth we are now missing in China, we prefer to keep our eyes on the oil price. These extreme moves can not be without consequence.

Many oil producers receive a fixed price for their oil as they covered their production with price insurance in the form of derivatives. With the current oil price, we just guess insurance providers paid out about 35 dollars a barrel to compensate the losses of the producers. Only for the US shale production this amounts roughly to 120 Million dollars a day. Somehow the financial sector has to cover these loses.

The US Energy Information Administration (EIA) stated in 2014 that most shale producers revenue has covered 75% of the production costs including initial investments, back then the oil price was about $95 a barrel. Even in 2014 this cast doubt on the profitability of US shale producers. Producers now claim they have lowered the production costs and are more efficient to reassure investors. But it is hard to believe they are now able to produce 50% cheaper. As investors are not buying this and start to flee the market, shale producers borrowing cost are starting to sky rocket, adding more pressure on the industry. Investors fear have already resulted in a spike in US junk bond rates. The energy sector accounts for about 15 percent of junk bond issuance. KKR has amortized 5 billion on two energy related bankruptcies. Restructuring of production companies will be inevitable.

Russian, Saudi and Norwegian sovereign wealth funds have used their profits to invest in US and European securities, like stocks and bonds. These funds see their cash inflow halted while profits start to turn into losses. The Norwegian sovereign wealth fund, one of worlds largest sovereign wealth fund, recorded a loss in the first quarter. Russia and Saudi Arabia need 100 dollars a barrel to get their budget balanced. The oil price is so low now these funds have to dis-invest. Saudi-Arabia’s postpone selling assets from it sovereign wealth fund, mainly US treasuries, as they chose to cover their budget deficit by issuing sovereign bonds themselves. Another sign the market being stressed.

Not only financial institutions selling assets to cover their oil related losses, add selling pressure to the market but also the decline of the share price of oil companies will be a drag on stock indices. Oil and oil related industries are part of nearly all big stock indices, a downturn in oil will in the end have its effect on these indices. The decline of major indices will have a negative effect on related ETF’s and comparable products. Most products that track indices are covered by stock portfolios. As investors start to buy these products, managers have to add stock to their portfolio in accordance with the index composition. If indices start to fall, ETF’s and comparable products start to under-perform, investors will sell these products forcing portfolio managers to sell stocks, adding extra pressure to the stock markets at large.

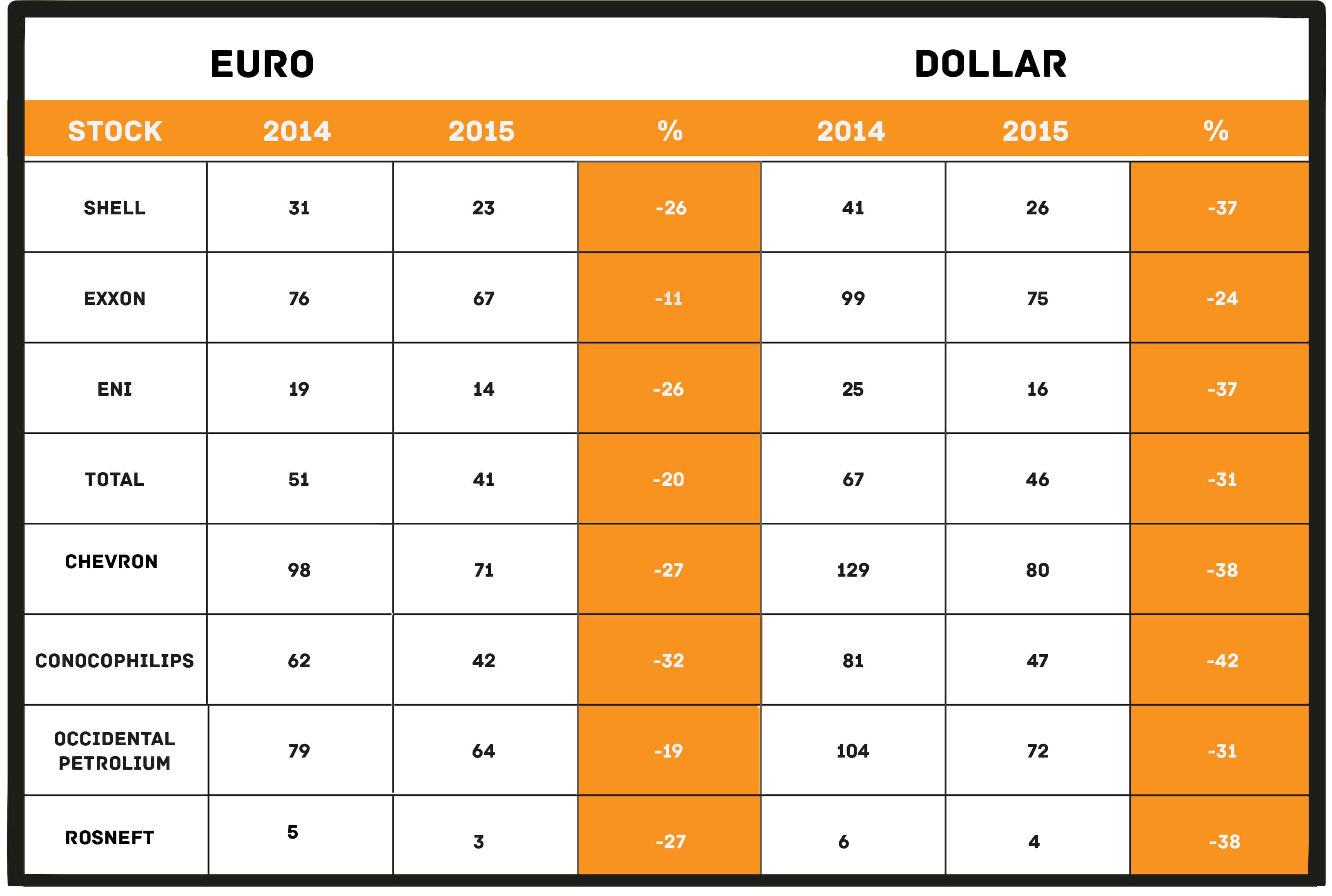

Table 1. Oil share prices in august 2014 compare to august 2015. Prices in Euro’s and Dollars.

In 2013 we informed our clients that oil was in an extreme bubble. From our analyses we expect the oil price will rebound after producers have been forced out of the markets. In the processes of re-balancing we are expecting that to much capacity will be eliminated, pushing oil in a new bubble. For the moment we are expecting oil producers to start to minimize their loses by producing even more oil. The oil crisis has just to begin. There is much volatility but for the moment we see no reason to invest in oil or oil stocks as the real carnage has not started yet.